Suffice it to say, a lot has happened this quarter.

On January 3rd, the United States executed Operation Absolute Resolve to arrest President Nicolas Maduro and his wife, Cilia Flores. Later that month, President Trump announced his intent to nominate Kevin Warsh to succeed Jerome Powell as Chair of the Board of Governors of the Federal Reserve System. In February, the Supreme Court ruled that the International Emergency Economic Powers Act (IEEPA) does not grant the executive branch authority to impose taxes or duties, officially defining tariffs as a form of taxation and, thus, striking down the President’s unilateral imposition of tariffs. In response, the administration utilized Section 122 of the Trade Act of 1974 to reimpose tariffs for 150 days. Shortly thereafter, the United States launched Operation Epic Fury, eliminating Supreme Leader Ayatollah Ali Khamenei and conducting vast military operations in the region. All the while, investors have become concerned with AI disruption fears, resulting in significant price action in multiple sectors, but particularly regarding Software as a Service companies, earning the portmanteau of “The SaaSacre”. That fear has spilled over into the world of private credit as investors have become concerned that the debt issued by the aforementioned software companies needs to be repriced, eliciting redemptions in illiquid vehicles. Private credit funds have largely capped those redemptions, further perpetuating liquidity concerns.

Each of these events, in and of themselves, would be significant enough to dedicate an entire quarterly letter to. Recapping all of them would demand an uncommon endurance of the reader. So, rather than attempting to do so, a more productive use of this quarter’s letter may be to discuss how our investment approach is suited and applied to navigate such environments. For Q3 2024, I wrote a letter titled “Headlines and Heuristics: Investing Through the News Cycle” which broadly spoke to the advantage of remaining committed to a disciplined investment philosophy amidst a period of dramatic headlines. Perhaps the most noteworthy conclusion of that piece was,

It remains our job, at Harris Associates, to see through these impending headlines (aye, not ignore), understand the impact to cash flows, and evaluate the resulting discrepancy between price and value.

It is my hope that, this quarter, a more tangible example can help illuminate the parenthetical phrase, “aye, not ignore,” to help illustrate how we interpret changing inputs and, subsequently, how those inputs result in investment decisions made for your portfolio.

You’ve likely heard us explain that “fairly valued” is when price is equal to our estimate of intrinsic value and, further, that we estimate the intrinsic value of a business based on an estimate of “normal”. But what exactly does that mean? How does one price for normal amidst events that feel anything but?

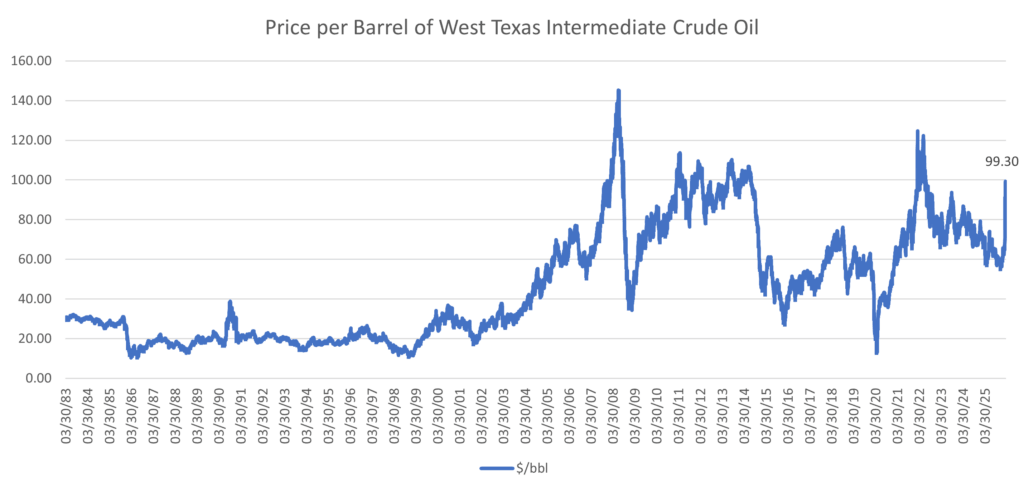

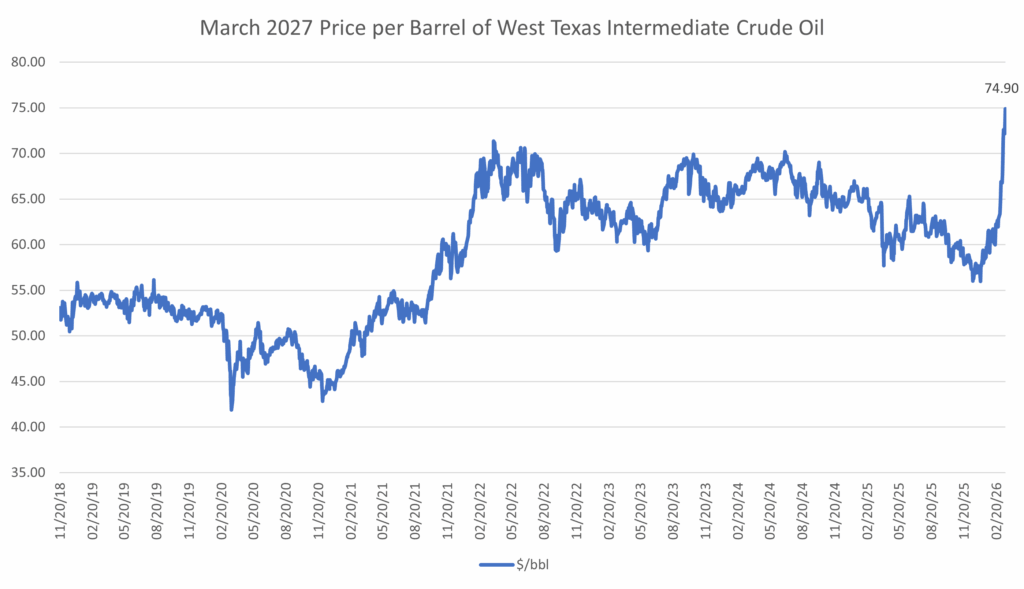

Apropos to the current environment might be an example of estimating the value of an oil exploration and production (E&P) company. Being in the business of selling oil, to do so requires an assumption of the “normal” price of oil per barrel. What is the normal price of a barrel of oil? The commodity is notoriously volatile – subject to economic sentiment, geopolitical events, etc. Since as recently as January 1st, 2020, the commodity has traded as low as $6.50 per barrel, during the height of pandemic fears, and as high as $120, in response to the current conflict in Iran. As of the writing of this letter, current prices are hovering around $100. Should $100/bbl be considered normal? Our opinion would be – at this moment – no. There are identifiable and understandable geopolitical events that have restricted supply, pushing up prices. In fact, the market, more or less, agrees. Looking at the current price for a barrel of oil that will trade one year from now, Mr. Market believes oil prices will be somewhere around $75 (and continue to decline further out into the future). This is, likely, a much more realistic estimate of normal.

Source: FactSet

Source: FactSet

A quick aside: These prices reflect the current market environment at the time of this writing (late March). With the situation in the Middle East rapidly changing, they are subject, and highly likely, to change. That being said, for illustrative purposes, they serve as a useful example.

Consider for a moment – in isolation – the difference in value, assuming a constant discount rate, that would occur from changing the assumption of normal oil prices from $75/bbl to $100/bbl. A hypothetical and overly simplified (i.e., no associated costs) E&P company has, say, a single barrel to sell per year for the next 10 years and, further, that we assume that the price of oil over the next 10 years will be $75. If we increase that assumption to $100, the value of the entire company increases a commensurate amount: 33%! A stock price reaction in line with the change in value, in this case, would be completely rational. If the stock price increased 33% (equal to the increase in value), then the discount to intrinsic value that existed prior to the change in oil prices would persist (and, further, in the same magnitude). Our response would likely be no action despite the significant increase in price. In this simplified scenario, there has been no change in the discount to intrinsic value, thus the investment – in isolation – is as attractive at $100/bbl as it was at $75/bbl (albeit with a welcomed jump in price!).

However, let’s consider the same hypothetical company, but a more pragmatic path of oil prices, i.e., closer to the path as predicted by Mr. Market. Rather than increase the assumption to $100 for each of the remaining 10 years, what if we assume prices increase to $100 for one year and then, subsequently, fall to $75 for the remaining nine. Assuming an arbitrary discount rate of 10%, the value of the company would increase 5%. The increased cash flow next year (when the company can sell their barrel at $100 vs. $75), has real value to the shareholder and, thus, increases the estimate of intrinsic value. But because one year from now the assumption is that oil prices revert to “normal”, the value increase is far shy of the 33% we saw prior – when oil prices remained elevated for all ten years.

As of the time of this writing, the State Street SPDR Oil & Gas Exploration & Production ETF (a decent proxy for E&P stock prices more broadly) has increased ~15% since the beginning of the conflict – far less than the increase in the price per barrel of oil. A possible inference could be that the market has, rationally, assumed that these oil prices will not prevail in perpetuity. However, if our hypothetical view of “normal” has not changed, and we follow the more pragmatic path of adjusting our company valuations for one year of higher cash flows, our estimate of intrinsic value increases closer to 5%. As a result, stock prices have risen faster than our estimate of intrinsic value (15% vs. 5%), and the discount to intrinsic value has shrunk! The investment opportunity has, therefore, become less attractive (again, in isolation).

As is the case with any investment, as the stock price converges to our estimate of intrinsic value, our discipline is to sell (and vice versa). In response, you can expect to see such actions taken in your portfolio.

Importantly, valuing businesses based on “normal” does not mean reacting to consequential events with a proverbial shrug – as if to say, “These are not normal events, and thus do not impact value.” Quite the contrary. It means actively updating our estimates, but for only as far as we can comfortably see (one, maybe two years max) and maintaining our estimate (if appropriate) of normal beyond that. The critical insight is that adjusting the next one or two years of cash flows does not – typically – change value as much as equity prices move in response to dramatic, newsworthy events. That distinction is where discounts to value expand or contract, eliciting trading activity.

Predicting the future is hard (this quarter reminded us all of that!). Doing it many times over, across varying industries, borders on the impossible. Yet, investing is inherently an exercise in just that. How do we responsibly reconcile the two?

In my recent readings I stumbled across the phrase, “epistemic humility.” As is typical of our modern era, I asked AI what it means:

“epistemic humility” — The intellectual virtue of recognizing the limitations of one’s own knowledge, acknowledging that beliefs are provisional, fallible, and subject to revision. It involves an open-minded, self-questioning attitude toward personal biases, preventing arrogance and fostering ongoing learning.

At Harris, we practice epistemic humility via our application of “normal,” admitting that we do not possess a competitive advantage in our ability to predict the future many years out. Doing so forces us to acknowledge that our long-term predictions are provisional and fallible. Simultaneously, we are continuously making revisions, updating our short-term assumptions so as to reflect the economic environment in our valuation estimates.

It is my hope that this quarter’s letter helped to bridge the gap between the abstract summary of our investment philosophy and how our discipline is applied.

As always, we thank you for entrusting us with your investment assets and your continued support. Lastly, the best compliment we can receive is a referral from a satisfied client. We appreciate your referrals and handle them with the utmost care.

Past performance is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. The investment return and principal value vary so that an investor’s shares when redeemed may be worth more or less than the original cost.

The specific securities identified and described in this report do not represent all the securities purchased, sold, or recommended to advisory clients. There is no assurance that any securities discussed herein will remain in an account’s portfolio at the time one receives this report or that securities sold have not been repurchased. It should not be assumed that any of the securities, transactions, or holdings discussed herein were or will prove to be profitable.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy, sell or hold a security or an investment strategy, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

The information, data, analyses, and opinions presented herein (including current investment themes, the portfolio managers’ research and investment process, and portfolio characteristics) are for informational purposes only and represent the investments and views of the portfolio managers and Harris Associates L.P. as of the date written and are subject to change without notice. This content is not a recommendation of or an offer to buy or sell a security and is not warranted to be correct, complete or accurate. Certain comments herein are based on current expectations and are considered “forward-looking statements”. These forward looking statements reflect assumptions and analyses made by the portfolio managers and Harris Associates L.P. based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Actual future results are subject to a number of investment and other risks and may prove to be different from expectations. Readers are cautioned not to place undue reliance on the forward-looking statements.

The S&P 500 Index is a float-adjusted, capitalization-weighted index of 500 U.S. large-capitalization stocks representing all major industries. It is a widely recognized index of broad, U.S. equity market performance. Returns reflect the reinvestment of dividends. This index is unmanaged and investors cannot invest directly in this index.

All information provided is as of 03/31/2026 unless otherwise specified.