Updated from original posting.

The outlook for the European banks owned in the Oakmark International Fund has moderated given the impact of the coronavirus to the global economy. While we are not experts on the coronavirus, we have a deep investment team that is experienced and practiced at valuing businesses. This disciplined approach helps us identify opportunities during times of crisis and increased volatility. We continue to believe we are positioned in the strongest banks in the sector, including BNP Paribas, Credit Suisse Group, Intesa Sanpaolo, Lloyds Banking Group and Royal Bank of Scotland (RBS), given they are well capitalized and possess high profitability buffers.

Impact to intrinsic value

We are constantly stress testing our assumptions to determine the interest rate and economic sensitivity of our banks. To incorporate slower economic growth and reduced central bank interest rates, we are making three primary adjustments:

- Reducing base interest rates

- Lowering loan growth

- Increasing credit costs

Interest rates

We believe the coronavirus will impact interim cash flows as governments take austerity measures and expect these even lower base rates to persist for the short term. Our base case scenario is that rates remain lower for the next two years with an eventual return to pre-coronavirus levels in 2022. As a result of lower interest rates for potentially the next two years, we have brought down fair values by a few percentage points. In a lower for longer scenario, where these recently lowered rates persist for the next four to five years, our intrinsic value estimates could be reduced by an additional mid-single percent. Keep in mind that assumes no offsetting measures taken by management, including cost reduction measures, growing fee-based businesses and a rationalization of marginal competitors, a scenario we see as unlikely.

European banks have been operating in an environment with negative interest rates for some time now. Actions taken by our banks have produced positive returns as a result of adeptly reducing costs, investing in digital and repositioning their asset mix toward superior quality. For example, we’ve invested with CEO Antonio Horta-Osorio since his days at Banco Santander. We initiated a position in Lloyds, the U.K. leader in consumer banking, in December 2011 after his arrival because of Horta-Osorio’s strong operational and capital allocation track record. Under his leadership, Lloyds has improved its ROTE over the last eight years by reducing operating and credit costs that more than offset the headwinds from lower interest rates.

Asset quality

We believe the European banks are in a much stronger position to weather a potential credit downturn today than they have been during previous cycles. Tighter underwriting standards, higher capital levels, slower credit growth, and the absence of any obvious residential or commercial real estate bubbles all contribute to this relatively strong positioning. Governments across Europe are being very proactive in supporting small- and medium-sized enterprises and industries that are more exposed to the coronavirus, such as airlines and hotels.

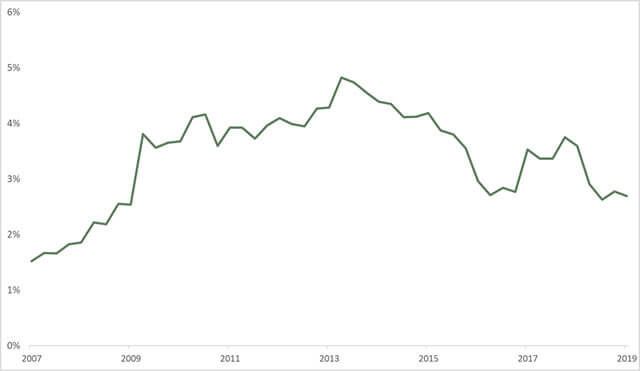

Going forward, we do assume increases in non-performing loans (NPLs) and bankruptcies of corporate clients of the European banks. Overall, we are now modeling in a double digit percent increase in both NPLs and credit costs for both FY2020 and FY2021. Because we believe our bank holdings have strong loan books with high levels of underlying profitability, we do not expect these short-term adjustments will be material to our valuations.

Figure 1: European Banks NPL Ratio

Source: European Central Bank

Liquidity

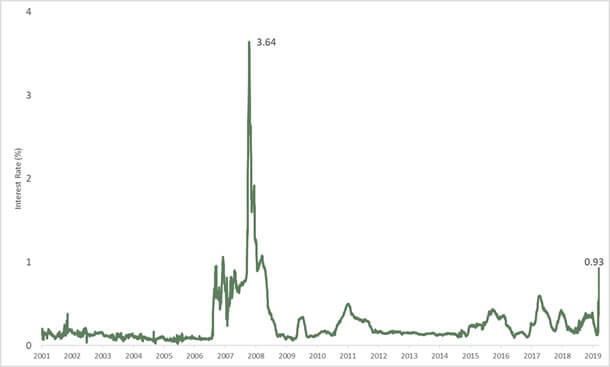

The European Central Bank (ECB) is taking steps to ensure liquidity. The ECB reintroduced LTRO, a cheap loan scheme that was first used in 2011, with the aim to eliminate potential Euro liquidity strains. In the first LTRO auction this week, €109 billion was taken up by 110 banks. We believe this will be an effective backstop for banks as funding conditions worsen. We are monitoring three month Libor–OIS spreads. While they have widened in the past week, they remain well off the global financial crisis highs.

Figure 2: 3 Month USD LIBOR–OIS Spread

Source: Bloomberg

While we believe government actions to provide liquidity are the correct course of action, we are also comforted by the significant improvement in bank liquidity coupled with a reduced reliance on higher risk wholesale funding sources. Autonomous,1 an independent research firm focused on financial institutions, estimates European banks aggregated loan-to-deposit ratios fell from 125% in 2008 to less than 100% currently. In addition, we believe that our bank holdings possess lower liquidity risk than the average given superior franchises coupled with better business models.

Capital

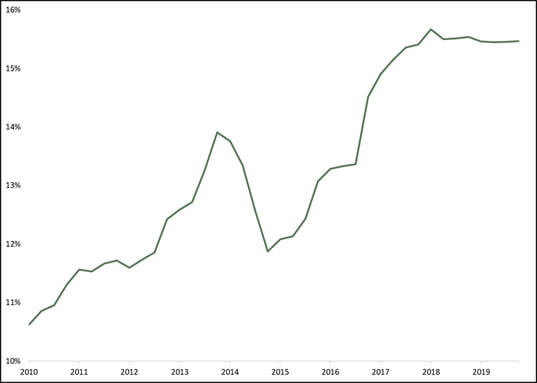

When the large global banks entered the global financial crisis they were unprepared for the situation with a comparable CET1 capital position of only 3.8% in 2007 versus 13.4% at the end of 2019.1 Today, capital levels are effectively 3.5x higher than before the start of the 2008 financial crisis and many of our banks possess either higher capital levels or more diversified/lower risk business models than the average.

While regulations and rules stiffened over the last decade, central banks in Europe and the United Kingdom are now reducing these counter cyclical buffers to help support the economy. The Bank of England (BOE) recently announced reduced capital requirements for both RBS and Lloyds, leaving them both way over-capitalized.

Figure 3: European Banks Core Tier 1 Capital Ratio

Source: European Central Bank

Given the spread of the virus within Italy, it appears Intesa will be the most impacted by this as it stands now. However, Intesa has a ~460bps capital buffer over required capital, positioning the company to handle potential spikes in credit costs.

Figure 4: Oakmark International European Bank Capital Levels

| As of March 17, 2020 | 2007 Core Tier 1 Ratio | 2019 Core Tier 1 Ratio |

|---|---|---|

| BNP Paribas | 7.3% | 12.4% |

| RBS | 7.3% | 16.2% |

| Lloyds | 8.1% | 13.8% |

| Intesa Sanpaolo | 5.9% | 14.1% |

| Credit Suisse | 11.1% | 12.7% |

Source: Harris Associates

Widening value gap

As is often the case, share prices of our banks have fallen by approximately 45% over the last month. We believe a value gap is widening. When this occurs, you can expect us to purchase the names with the most upside to intrinsic value, essentially de-risking our portfolio.

Figure 5: Oakmark International Financial holdings valuation update

| As of March 17, 2020 | Stock Price Total Return QTD | Price to Tangible Book Value FY1 | Price to Earnings Ratio FY1 | Dividend Yield 2020E |

|---|---|---|---|---|

| BNP Paribas (€) | -45% | 0.4x | 5.5x | 10.6% |

| RBS (£) | -45% | 0.5x | 9.2x* | 9.1% |

| Lloyds (£) | -43% | 0.7x | 5.5x | 10.0% |

| Credit Suisse (CHF) | -48% | 0.4x | 4.0x | 4.6% |

| Intesa Sanpaolo (€) | -38% | 0.5x | 5.6x | 12.6% |

Source: Harris Associates estimates. *RBS P/E adjusted for one-time items.

When the uncertainty starts to wane in time, we believe the European financials can provide strong total returns for our shareholders. Thank you for your continued confidence and patience.

The holdings mentioned comprise the following percentages of the Fund’s total net assets as of 03/31/2021:

| Security | Oakmark International Fund |

|---|---|

| BNP Paribas | 3.8% |

| Credit Suisse Group | 3.2% |

| Intesa Sanpaolo | 4.1% |

| Lloyds Banking Group | 4.7% |

| Royal Bank of Scotland | 0% |

Portfolio holdings are subject to change without notice and are not intended as recommendations of individual stocks.

1Autonomous Research. (2020). European Banks – What’s Priced In.

The Fund’s portfolio tends to be invested in a relatively small number of stocks. As a result, the appreciation or depreciation of any one security held by the Fund will have a greater impact on the Fund’s net asset value than it would if the Fund invested in a larger number of securities. Although that strategy has the potential to generate attractive returns over time, it also increases the Fund’s volatility.

Investing in foreign securities presents risks that in some ways may be greater than U.S. investments. Those risks include: currency fluctuation; different regulation, accounting standards, trading practices and levels of available information; generally higher transaction costs; and political risks.

The information, data, analyses, and opinions presented herein (including current investment themes, the portfolio managers’ research and investment process, and portfolio characteristics) are for informational purposes only and represent the investments and views of the portfolio managers and Harris Associates L.P. as of the date written and are subject to change and may change based on market and other conditions and without notice. This content is not a recommendation of or an offer to buy or sell a security and is not warranted to be correct, complete or accurate.

Certain comments herein are based on current expectations and are considered “forward-looking statements”. These forward looking statements reflect assumptions and analyses made by the portfolio managers and Harris Associates L.P. based on their experience and perception of historical trends, current conditions, expected future developments, and other factors they believe are relevant. Actual future results are subject to a number of investment and other risks and may prove to be different from expectations. Readers are cautioned not to place undue reliance on the forward-looking statements.